The Thursday Report 2.27.2014 – Giraffe Beers, Couple Agmts and Seminars

Whammed and Spammed

Economic Relationship Agreements for Same-S*x Couples

SCIN, SCRAM, ANNUITY or SCGRAT – Don’t Leave Your Clients with Short Life Expectancies Flat

Seminar and Webinar Announcements: Ave Maria School of Law Estate Planning Conference and Strafford JEST Webinar

The Balanced Scorecard of an IPA, an article by Dr. Pariksith Singh

We welcome contributions for future Thursday Report topics. If you are interested in making a contribution as a guest writer, please email Janine Gunyan at Janine@gassmanpa.com.

This report and other Thursday Reports can be found on our website at www.gassmanlaw.com.

Special thanks to Anne Sunne Freeman for her testimonial for the Thursday Report:

Good morning Alan,

I just wanted to thank you for the tax update in your newsletter this week. I am not a tax attorney and I found it very informative. You are awesome!

Take care,

Anne Sunne Freeman

Why are we saying S*X? Because when we say the other word we get:

Whammed and Spammed!!

Has your Thursday Report been in internet computer land?

Our series of information on planning for unmarried (same-s*x) couples caused a great many of our subscribers computers to automatically spam the Thursday Report because of the word that has the letter “X” in it.

You may therefore have unread Thursday Reports in your spam folder. SPAM goes great with Kentucky Fried Chicken, but the shelf-life of SPAM is longer, so please take a look at the Thursday Reports you have not gotten to, or send them to your mother-in-law for her birthday.

If you have been spammed and would like to keep receiving the Thursday Report please click here to send an email to Janine Gunyan at Janine@gassmanpa.com indicating that you would still like to receive the report.

Economic Relationship Agreements for Same S*x Couples

By: Alan S. Gassman, Esq. and Danielle Creech, Esq.

The following is a continuation of our sharing sections from the book we are writing entitled The Florida Advisors Guide to Counseling Same S*x Couples in 2014. Alan Gassman will be presenting these materials at the Wealth Council Florida Forum on Friday, March 21, 2014 in Orlando, Florida. More details regarding that seminar appear below, and all suggestions are welcome.

DIVORCE AND DOMESTIC PARTNERSHIP AGREEMENTS

Divorce is still very uncharted territory with respect to same-s*x marriages. Because many states do not recognize same s*x marriages, couples who got married in a state that was not their state of residence may find that their state of residence will not grant them a divorce. Thus, if the partners have a disagreement on how to split up the marital assets the court system will have no available remedy. Although states such as California and Massachusetts, which have done large numbers of same s*x marriages for couples across the country, do not have residency requirements for marriage, they do have residency requirements for divorce.1

The divorce prohibition in certain states could change in the not too distant future, and, if so, alimony and property settlement rights might date back to when the couple was originally married, as opposed to dating back to when the state legislature and governor might sign such legislation into existence.

When a same s*x couple lives in a state that does not recognize same s*x marriage, but is validly married in another state, they can consider a Domestic Partnership Agreement. A Domestic Partnership Agreement, in a way, works like a prenuptial agreement, for it is a contract between partners that provides the court a way to divide up the marital assets and even create support rights between partners.2 While there is no guarantee that a court in a non-recognition state will uphold same s*x domestic partnership agreements, it does not hurt to draft one to show a couple’s intent.

One Florida appellate court has upheld domestic partnership or cohabitation agreements between unmarried same s*x couples.3 The Fourth District Court of Appeals, in the case of Posik v. Layton in 1997, found that even though Florida prohibited same s*x marriages, it did not prevent a domestic partnership agreement from being legally enforceable.4 A copy of the decision can be found in the Appendix, and includes the following statement:

“By prohibiting same-s*x marriages, the state has merely denied homos*xuals the rights granted to married partners that flow naturally . . . But the State has not denied these individuals their rights to either will their property as they see fit nor to privately commit by contract to spend their money as they choose.”5

Thus, while we are unsure if premarital agreements will be upheld in Florida, privately contracted agreements, such as a Domestic Partnership Agreement, will most likely be upheld if properly drafted and implemented.

Example

Assume that things do not work out between Sam and George, and after four years of marriage they decide to get a divorce. They have a prenuptial agreement, and they were married in Massachusetts. Neither George nor Sam ever resided in Massachusetts, and to get married, they were not required to do so.

They go to the Florida courts to request a divorce, but they are denied. The judge determines that because they were married in a union that the state of Florida does not recognize, the state of Florida cannot grant their divorce.

Unfortunately, Massachusetts does have residency requirements for divorce. If the grounds for divorce occurred outside of the state (in this case, they occurred in Florida), then one spouse must be a Massachusetts resident for one year before the state will move forward with divorce proceedings.

As neither George nor Sam have any ties to Massachusetts, neither of them want to reside there in order to get the divorce. They may choose to separate without the legal divorce, but this has repercussions as well. If either of them remarries, it may technically be considered bigamy, though it is unclear as to whether this would apply in a state that does not recognize the marriage in the first place. Many states are currently facing lawsuits on this issue, and the legal community should keep an ear to the ground with respect to this issue.

Many attorneys for same s*x marriage are recommending prenuptial agreements for same s*x couples. This is particularly important as many couples who plan to or have recently married are older and more established, and therefore have more of their own independent wealth to protect in the event of divorce. On the other hand, if a couple lives in a jurisdiction that does not recognize same s*x marriage, they may not be entitled to a marital division of assets in the event of a split and the prenuptial agreement may not be valid.

Thus, a domestic partnership agreement is the most secure way of determining how a couple will divide assets in the event of separation in a non-recognition state.

The Domestic Partnership Agreement can contain many terms, and there are many considerations associated therewith.

Some important factors are as follows:

1. Summarize the economic reasons for the agreement, particularly if one partner is making career sacrifices to raise a child or children, or to concentrate on homemaking.

2. Follow the standards that apply to Florida postnuptial agreements with respect to the following:

a) Full and complete disclosure.

b) Strongly urging each party to have separate independent legal counsel.

c) Making sure that there is no duress or appearance of duress- sign before wedding invitations or any similar situation occurs.

3. If the parties are not married, consider the tax impact of pseudo-alimony payments and property settlement transfers that might occur. Would it be against public policy for the agreement to require that the parties become married upon the request of either spouse, in order to have the tax advantages that would apply in the event of a divorce?

4. Consider a geographic living limitation requirement if and when the parties have a common child or children.

5. Beyond simply agreeing that Florida law should apply as if the parties were married from a date agreed to, consider the following alterations to Florida law:

A. Binding private arbitration in lieu of public litigation, to the extent legally enforceable.

B. Allow either party to request bifurcation of arbitration proceedings, so that issues such as the enforceability of the agreement and specific provisions thereof can be determined by the arbitrator before going to the next step of adding discovery and arbitration hearings on legal rights that may not apply if the agreement is upheld or denied.

6. Consider attorney fee provisions in lieu of simply having the spouse more able to pay be responsible for all fees.

7. Consider requiring initial representation by collaborative lawyers to the extent legally enforceable.

FLORIDA LITIGATION – WILL THE TIDE TURN HERE?

Six couples in Miami, Florida have filed a lawsuit demanding that they be allowed to marry their same s*x partners.1 The suit was filed on January 21, 2014. A copy of the complaint filed by these couples can be found in the Appendix and includes a number of compelling arguments that may be successful to require Florida law to recognize and respect same s*x marriages. This could apply retroactively to same s*x couples who have been married in jurisdictions outside of Florida that recognize same s*x couple marriages.

The Complaint filed in this matter contains the following statements:

9. In the not so distant past, the majority of states, including Florida, had laws prohibiting marriage between people of different races. Until 1967, the Constitution and laws of Florida barred marriages between white and black persons. See former Art. 16, § 24, Fla. Const.; former Fla. Stat. § 741.11 (repealed by Fla. Laws 1969, ch. 69-195, § 1). The Supreme Court of the United States held such exclusions from marriage to be unconstitutional in Loving v. Virginia, 388 U.S. 1, 12 (1967), declaring: “The freedom to marry has long been recognized as one of the vital personal rights essential to the orderly pursuit of happiness by free men.” See also Van Hook v. Blanton, 206 So.2d 210 (Fla. 1968) (granting writ of mandamus declaring Florida anti-miscegenation laws invalid in light of Loving).

11. Marriage contributes to the happiness, security and peace of mind of countless couples and their families, and to the stability and well being of society. Florida, like other states, encourages and regulates marriage through hundreds of laws that provide benefits to, and impose obligations on, married couples. Florida in turn enjoys the well-established benefits that marriage brings: stable, supportive families that contribute to both the social and economic well-being of Florida. “There can be no doubt that the institution of marriage is the foundation of the familial and social structure of our Nation. . . .” Posner v. Posner, 233 So. 2d 381, 384 (Fla. 1970). Marriage means many things, including “cohabitation, the founding of a home, affections, and companionship,” and is premised on the reality that “we depend on each other during the changing vicissitudes of life.” Orr v. State, 176 So. 510, 514 (Fla. 1937).

12. When Florida withholds a marriage license from a same-s*x couple, Florida circumscribes individuals’ basic life choices, classifies persons in a manner that denies them the public recognition and myriad benefits of marriage, prevents couples from making a legally binding commitment to one another and from being treated by the government and by others as a family rather than as unrelated individuals, and harms society by burdening committed families and preventing couples from being able to fully protect and assume responsibility for one another and their children.

13. Florida’s exclusion of same-s*x couples from marriage violates the Due Process Clause and the Equal Protection Clause of the Fourteenth Amendment to the United States Constitution. Florida’s exclusion deprives same-s*x couples of their fundamental right to marry; infringes upon their constitutionally protected interests in liberty, dignity, privacy, autonomy, family integrity, and intimate association; and deprives them of equal protection of the laws.

The Complaint goes on to explain that each of the plaintiffs satisfy all requirements that would apply under Florida law to become married if they were opposite s*x couples, and then explains the history of Florida laws barring same-s*x couples, as follows:

27. In 1977, the Florida legislature amended Fla. Stat. § 741.04 to expressly limit the issuance of marriage licenses to opposite-s*x couples. Section 741.04 states in relevant part:

No county court judge or clerk of the circuit court in this state shall issue a license for the marriage of any person unless there shall be first presented and filed with him or her an affidavit in writing, signed by both parties to the marriage, providing the social security numbers or any other available identification numbers of each party, made and subscribed before some person authorized by law to administer an oath, reciting the true and correct ages of such parties; unless both such parties shall be over the age of 18 years, except as provided in s. 7410405; and unless one party is a male and the other party is a female. (Emphasis added.)

28. In 1997, in response to the possibility that some states might permit same-s*x couples to marry, the Florida legislature enacted Fla. Stat. § 741.212 to again prohibit marriages between same-s*x couples. That statute provides:

(1) Marriages between persons of the same s*x entered into in any jurisdiction, whether within or outside the State of Florida, the United States, or any other jurisdiction, either domestic or foreign, or any other place or location, or relationships between persons of the same s*x which are treated as marriages in any jurisdiction, whether within or outside the State of Florida, the United States, or any other jurisdiction, either domestic or foreign, or any other place or location, are not recognized for any purpose in this state.

(2) The state, its agencies, and its political subdivisions may not give effect to any public act, record, or judicial proceeding of any state, territory, possession, or tribe of the United States or of any other jurisdiction, either domestic or foreign, or any other place or location respecting either a marriage or relationship not recognized under subsection (1) or a claim arising from such a marriage or relationship.

(3) For purposes of interpreting any state statute or rule, the term “marriage” means only a legal union between one man and one woman as husband and wife, and the term “spouse” applies only to a member of such a union.

29. In 2008, Florida amended its Constitution to include a provision excluding same-s*x couples from marriage. Article I, Section 27 of the Florida Constitution provides:

Insomuch as marriage is the legal union of only one man and one woman as husband and wife, no other legal union that is treated as marriage or the substantial equivalent thereof shall be valid or recognized.

The counts in this Complaint are as follows:

Count One

Violation of the Due Process Clause of the Fourteenth Amendment to the United States Constitution (brought pursuant to 42 U.S.C. § 1983)

Count Two

Violations of the Equal Protection Clause of the Fourteenth Amendment to the United States Constitution (brought pursuant to 42 U.S.C. § 1983)

A. Discrimination Based on S*xual Orientation

B. Discrimination Based on S*x

C. Discrimination with Respect to Fundamental Rights and Liberty Interests Secured by the Due Process Clause

D. Entitlement to Declaratory Relief

Legal counsel for the plaintiffs included Nancy J. Faggianelli, Sylvia H. Walbolt, Luis Prats, Jeffrey Michael Cohen, Cristina Alonso of the Carlton Fields Jorden Burt, P.A. law firm in Tampa and Miami.

SCIN, SCRAM, ANNUITY, or SCGRAT

Don’t Leave Your Clients with Short Life Expectancies Flat

Planning for Clients with Short Life Expectancies After Davidson and CCA 2013-30-033

By: Alan S. Gassman and Kenneth J. Crotty

The following, or an improved version thereof, will soon be published with Leimberg Information Services.

Primary Implications of the Limited Choices That Planners Have to Assist Taxpayers – the Good News Is That the Choices and Solutions Are Understandable and Easily Implemented.

EXECUTIVE SUMMARY:

Since the Tax Court decision of Estate of Moss v. Comm’r in 1980 and the issuance of Treasury Regulation § 1.1275-1(j) in 1998, estate tax planners have used self-cancelling installment notes (SCINs) to save millions of dollars of estate taxes for taxpayers whose life expectancy may be shorter than that assumed under the 2000CM Mortality Table promulgated by the Treasury Department under Publication 1457. In the recent CCA 2013-30-033, the IRS has taken the position in the Davidson case that clients with shorter than average life expectancies may not rely on the 2000CM Mortality Table to determine their life expectancy for the purpose of valuing the SCIN and may make taxable gifts when the sale occurs if they do rely on the 200CM Mortality Table. To reduce the possible gift tax exposure for clients, practitioners using SCIN with clients who have reduced life expectancies may want to use the SCGRAT technique described below.

FACTS:

The industry practice for most well versed practitioners has been that the 2000CM Mortality Table can be used when the taxpayer has a better than 50% chance of living at least one year at the time that the SCIN or private annuity arrangement is entered into.

In order to avoid incurring income tax on the sale of assets for a SCIN or private annuity, most arrangements have entailed having an irrevocable trust established to be separate and apart from the taxpayer for federal estate tax purposes, while being disregarded for income tax purposes so that there is no income on the sale and no interest or Internal Code Revenue § 72 income recognized by the taxpayer as payments are received by the taxpayer from the trust during the taxpayer’s lifetime.

Treasury Regulation § 25.7250-3(b)(2)(i) was enacted to implement the “probability of exhaustion test” which generally provides that if the entity purchasing assets for a private annuity is not capitalized with sufficient assets to enable the trust to make the scheduled private annuity payments until the Grantor reaches age 115, assuming a market rate equal to what is known as the 7520 rate which is equal to 120% of the Federal midterm rate in effect under § 1274(d)(1) for the month when the transaction is entered into, rounded up to the nearest 2/10ths of 1%.

Because of the difficulty of satisfying the probability of exhaustion test, especially in periods of low interest rates, most estate tax planners have recommended the use of SCINs, which are not subject to that test. A commonly used planning industry rule of thumb has been that a trust purchasing assets from a Grantor in exchange for a SCIN should have a positive net worth equal to 10% or more of the value of the assets purchased in order to be considered a separate and viable entity for estate tax planning purposes.

When trusts do not have sufficient assets to pass the probability of exhaustion test or the “10% rule of thumb” described above then it is common to have beneficiaries or affiliated entities guarantee the note or the private annuity in order to meet the applicable test, the 10% test for a SCIN or the probability of exhaustion test for a private annuity.

Treasury Regulation § 25.7520-3(b)(3)(I), which states that the 2000CM Mortality Table can be used when the person whose life controls the document has better than a 50% chance of living at least one year, applies explicitly to private annuities.

Many leading commentators, including Howard Zaritsky and Ronald D. Aucutt, have concluded that most likely this regulation applies to SCINs, because in form and content a SCIN constitutes a series of payments over time that can in substance be exactly the same as a private annuity contract.

The Service has strongly disagreed with this approach, but has waited over 18 years since the enactment of the above-referenced Treasury Regulation and notwithstanding annual and continuing industry and leading treatise literature to the contrary, on the occasion of the death and estate tax return audit of William M. Davidson to challenge this approach, whereby over $1,000,000,000 of estate tax is being assessed by the Service (constituting over 25% of the total estate taxes that the U.S. government would receive for a given calendar year) as the result of Mr. Davidson having sold a large percentage ownership in the Detroit Pistons basketball team and other assets in exchange for multiple SCINs when Mr. Davidson is said to have been in failing health.

The Service further threw the gauntlet down in front of the estate tax planning industry by publishing CCA 2013-30-033 on August 5, 2013, as an IRS Chief Counsel Advice which concludes that a SCIN will be worth substantially less than its face amount if a willing buyer would pay a willing seller less than the face amount if there was open market negotiation for the note.

In other words, if Mr. Davidson sold $1,000,000,000 worth of assets for a $1,000,000,000 SCIN then the trust that sold the note would only be able to receive $300,000,000 pursuant to an auction of the note at an event where every willing buyer received notice of the auction. Mr. Davidson would then have made a $700,000,000 gift and he would be subject to $280,000,000 worth of estate tax, enough to purchase two F-35 fighter jets.

What is a planner to do now when a wealthy client has a short life expectancy – SCRAM, go flat or SCGRAT?

COMMENTS:

Door Number 1

A private annuity arrangement could be entered into with family members, such as occurred in the 2012 Estate of Kite v. Commissioner case. If a private annuity is entered into where the parent sells assets to children, the children’s basis in the assets will be equal to the annuity payments made by the children. If the parent dies before receiving any annuity payments, such as what happened in the Kite case, the children would have a zero basis in the assets received and would face a 23.8% capital gains tax on the full value of the assets when they were sold.

Alternatively, the planner must face the probability of exhaustion test if a grantor trust is used that would quite possibly allow a stepped up basis for the assets.

The probability of exhaustion test may not apply, as discussed in the University of Miami Heckerling presentation by Lawrence Katzenstein , but there is a significant risk that the probability of exhaustion test will apply.

Door Number 2

Go with a SCIN, but understand the risk posed by CCA 2013-30-033 and the Davidson case that the Grantor could be making a significant taxable gift at the time the transaction was entered into.

Door Number 3

Do nothing, but accelerate planning with charitable donations, discounting, and other methods.

Door Number 4

The box where Carol Merrill is now standing.

Door number 4 is the bread slicer – or at least what we think is better than sliced bread – a SCIN arrangement that would allow any gift element to not be subject to gift tax and to instead be repayable to the Grantor by use of a grantor retained annuity trust arrangement.

Instead of selling the assets to a typical irrevocable grantor trust the taxpayer first establishes a limited liability company owned 100% by the Grantor and places the assets that are being “sold” into the LLC and also receives a SCIN from the LLC while verifying that the taxpayer has a better than a 50% chance of living at least one year.

The taxpayer also executes a grantor retained annuity trust agreement (GRAT) which provides that a percentage of the value of the Day 1 GRAT assets will be paid back to the Grantor each year for two years on the anniversary date of the GRAT being established.

The Grantor then transfers ownership of the LLC to the GRAT and hires a valuation firm to determine the value of the assets owned by the LLC.

If the valuation firm opines that the assets in the LLC are worth less than the face amount of the SCIN, then the LLC will be considered to have a negligible value, and the payments owed back to the Grantor will be very small. There should be some positive value even if the assets in the LLC are worth less than the SCIN because the owner of the LLC has no downside and at least some limited upside potential that the assets will grow in value and yield a net return exceeding the amount owed on the SCIN.

If the assets have a value exceeding the value amount of the SCIN then assuming the 7520 rate is 2.4%, then the excess amount multiplied by approximately 51.8% will be the amount of the annual payment that the GRAT will make to the Grantor, which may be in cash that the LLC can distribute to the GRAT or in the form of assets equal in value to such amounts that the LLC may distribute to the GRAT each year.

After the second annual payment, the LLC will be owned by the GRAT or an irrevocable “remainder trust” that the GRAT pours into after the second year.

The SCIN will typically be an interest only SCIN with a balloon payment at the end of the term of the note which will normally be just before the standard life expectancy of the individual on whose life the note is based as determined under 2000CM Mortality Table or the mortality table under Treasury Regulation § 1.72-9, Table V.

The 2000 CM Mortality Table will typically have a shorter life expectancy and it is therefore safer to use it. For example, for a 78 year old the life expectancy under the 200CM Mortality Table is 9.44 and the life expectancy under Treasury Regulation § 1.72-9, Table V is 10.63.

To determine the value of the SCIN, either the interest rate of the SCIN will be increased, the face amount of the SCIN will be increased, or the interest rate and the face amount of the SCIN can both be increased to the extent appropriate to satisfy actuarial assumptions which make the note equal in value to the assets sold so that the seller is compensated to take into account that the note will vanish on death. This can be determined based upon standard life expectancies under actuarial tables using software programs like Leimberg’s Number Cruncher and Larry Katzenstein Tiger Tables. The links to obtain these programs are as follows.

http://www.leimberg.com/products/software/numberCruncher.html

http://www.tigertables.com/

The need to value the assets held under the LLC is a substantial reason to use the GRAT when assets are hard to value or discounts will be applicable.

A GRAT must be funded in a single transfer and there is no authority for the ability to sell assets to a GRAT in exchange for a note at the time of funding.

This is why well respected commentators have suggested that an LLC that is disregarded for income tax purposes will first be funded by the Grantor and that the Grantor can receive a note back from the LLC in order to provide appropriate financial leverage for the arrangement.

Many taxpayers will want to have their remaining assets be under the amount that would require an estate tax return to be filed in order to reduce the paperwork, expenses, and delay in estate administration that results from having to file a federal estate tax return. A SCIN will not be considered to be an asset owned at the time of death for estate tax return threshold filing purposes.

However, in Estate of Moss v. Comm’r, 74 T.C. 1239 (1980) , the Tax Court held in favor of the estate….***See: Cain v. Comm’r, 37 T.C. 185 (1961)

Where a marital deduction devise or charitable disposition may facilitate avoidance of federal estate tax on the death of the Grantor when used in conjunction with the SGRAT, it can still be advisable to have GRAT assets pass to fund a marital devise or trust and/or a charitable devise as remainder beneficiaries of the GRAT so that a federal estate tax return using it is more clear that the assets passing to fund a marital devise will receive a stepped up basis if held by the taxpayer on death, but the advantage of not having to file a federal estate tax return may outweigh the risk of not receiving a stepped up basis on assets passing to fund a marital or charitable devise.

Another consideration is whether to maximize the use of the taxpayer’s generation skipping tax exemption makes the filing of a federal estate tax return worthwhile. Generation skipping tax exemption can clearly be allocated to a marital deduction trust that is funded from the Grantor’s estate or revocable trust that receives the payments from the GRAT.

Many clients will prefer to zero out the GRAT in order to avoid the need to file a federal gift tax return for the year that the SCGRAT is implemented. It may therefore be important to be sure that there are no gifts exceeding $14,000 per donee or any gifts that do not qualify for the annual gift tax exclusion for the year in which a gift tax return would be filed, although even if a gift tax return needs to be filed it seems likely that a zeroed out GRAT would not be considered to be a gift that would need to be reported on a gift tax return.

Sample charts demonstrating this SCRAT technique are attached.

CONCLUSION:

Utilizing a SCGRAT may be the best choice for practitioners who would like to use SCINs with a client who has a reduced life expectancy. If the Service successfully challenges the transaction and reduces the face value of the note by applying the willing buyer willing seller standard, by using the SCGRAT the value of the GRAT formed by the client should be increased. If the value of the GRAT is increased, then the payments from the GRAT to the client will be increased. As a result, there should not be any additional gift tax liability for the client.

Seminar and Webinar Announcements

Ave Maria is Closer Than Korea

Ever wanted to go to Korea? This is not a good time to go to North Korea, but consider Naples. Not Naples, Italy, of course, but Naples, Florida.

You can attend the Ave Maria School of Law Estate Planning Conference (don’t miss breakfast because we are a breakfast sponsor) on Friday, April 25, 2014 and have your pick from over 10 sessions (many run concurrently). Please pick our session on Using Estate Planning Techniques to Optimize Family Wealth Preservation. We will be counting the people!

Not only that but you can then stay at the Ritz Carlton on Friday night and Saturday night for only $338 per room, and the courtesy van will take you to the Kentucky Fried Chicken located at 12225 Collier Blvd.,which is only 9 minutes from the Ritz Carlton.

Have buckets of fun in Naples, both for our session, and also choose from the following fantastic presentations and speakers:

7:30 am Registration Opens

8:00 am Breakfast (Co-Sponsored by Gassman, Crotty & Denicolo, P.A. – sorry no Kentucky Fried Chicken, mashed potatoes or gravy.)

8:15 – 8:30 am Welcome and Opening Remarks

Eugene R. Milhizer, Ave Maria School of Law President and Dean Jonathan Gopman, Office Managing Partners at Akerman LLP

8:30 – 9:30 am General Session: Income Taxation of Trusts and Estates

Speaker: William A. Snyder

9:30 am – 9:45 am Networking Break

9:45 am –10:45 am Concurrent Sessions:

Session 1: International Tax Planning and Asset Protection

Speakers: Jonathan Gopman and Kevin Carmichael

Session 2: Homestead Portability: Pitfalls, Opportunities, and Traps

Speaker: Barry A. Nelson

10:45 am – 11:00 am Networking Break

11:00 am – 12:00 pm Concurrent Sessions:

Session 1: Succession Planning for the Closely Held Business Upon Retirement or Death of the Principal

Speaker: Jerome M. Hesch

Session 2: Using Estate Planning Techniques to Optimize Family Wealth Preservation

Speaker: Alan S. Gassman

12:00 pm – 1:15 pm Lunch Presentation: Estate Planning Ethics

Speaker: Gregory T. Holtz

1:15 pm – 2:15 pm Concurrent Sessions:

Session 1: A Baker’s Dozen of My Top Favorite Planning Ideas That I’m Willing to Talk About

Speaker: Bruce Stone

Session 2: Pitfalls for Estate Planners

Speaker: Laird A. Lile

2:15 pm – 2:30 pm Networking Break

2:30 pm – 3:30 pm Featured Session: Domestic Asset Protection Trust Planning

Speaker: Al W. King, III

3:30 pm – 4:30 pm Estate Planning Power Panel Discussion and Cocktail Reception

Panelists: Al W. King, III, Bruce Stone, Barry A. Nelson, Alan S. Gassman and Jerome M. Hesch

Moderator: Christopher P. Bray

For additional information on the Ave Maria School of Law Estate Planning Conference please contact Karen Grebing at kgrebing@avemarialaw.edu or 239-687-5404.

Strafford JEST Trust Webinar Notice

Stafford Publications, Inc. has just put Alan Gassman and Christopher Denicolo together with noted author and tax thinker Edwin Morrow to speak on Tuesday, March 18 from 1:00pm-2:30pm EDT on JEST planning.

More about this webinar can be found in our Seminars and Webinars section below.

If you would like to register for this webinar with Strafford (they keep all of the money of course!) you can register by visiting: https://www.straffordpub.com/products/structuring-joint-exempt-step-up-trusts-emerging-tool-to-maximize-step-up-in-basis-2014-03-18 or call 1-800-926-7926 ext. 10 Ask for Joint Exempt Step-Up Trust on 3/18/2014 and mention code: ZDFCT.

The Balanced Scorecard of an IPA (Independent Practice Association)

By: Pariksith Singh, M.D.

How does one evaluate an IPA (Independent Physicians’ Association)? This is an important question not only in assessing its value for sale or acquisition but also to measure its success, review the implementation of strategy and identify its key functions and metrics. We have seen the sale of several IPAs in the recent past in Tampa Bay and an interest among physician entrepreneurs in creating IPAs and attempt to make a fast buck. In this endeavor, they seem to look only at the financial balance sheet or returns of the organization and forget the other measurements that are key in the appraisal of an IPA.

The Balanced Scorecard (BSC) is a concept first articulated in a 1992 Harvard Business Review article by Robert S Kaplan and David Norton. It comprises of four perspectives which are necessary to have a composite snapshot of the state of health of a business. These perspectives are :

1) The Financial Perspective

2) The Customer Perspective

3) The Business Process Perspective

4) The Learning and Growth Perspective

In the book ‘The Balanced Scorecard: You Can’t Drive a Car Solely Relying on a Rearview Mirror’, Kaplan later expanded on this approach. It is ‘estimated that at least 40% of the Fortune 1000 companies use this methodology’.

In my opinion, a BSC is the best way in which one can measure the pulse of an IPA, although given the specific nature of an IPA, certain new perspectives must be added. These additional perspectives should be:

1) The Regulatory Perspective

2) The Legal Perspective

3) The Brand Perspective

If an IPA deals with Medicare lives and federally-funded dollars, the regulatory aspect of its functioning assumes an even more critical metric for any violation can threaten its very existence. Such a perspective should include compliance with HIPAA, OSHA, Stark laws, anti-kickback statutes, fee-splitting, Balanced Budget Amendments, the Affordable Care Act, etc. In light of some IPAs losing their contracts with HMOs recently, such a tally becomes immediate and significant.

An IPA is nothing if not relationships and contracts. If contracts do not exist, the IPA has no foundation and its entire structure collapses. Thus, strong and compliant contracts that are transparent and clear with powerful disincentives for breach would be essential. Without such contracts in place with coherent and ethical legal counsel to back it up, an IPA would founder and be unable to grow. Whatever growth and profits are accomplished are tenuous and expose it to further danger and vulnerability. It is my recommendation that all fee including administrative and re-insurance expenses be properly disclosed and attested by affiliates at the time of induction to the IPA. It is also my belief that the liabilities to the business be considered as one of the most critical sections of the BSC, i.e., the number of lawsuits against the organization, the potential damages from such lawsuits, the confidentiality of its data and reports or their loss, the nature of competition and poaching of its affiliates, conflicts in its relationships with the HMOs and potential OIG (Office of Inspector General) investigations of its practices.

The Brand of an IPA is the ‘X’ factor, its mystique and inevitability, uniqueness and desirability, customer loyalty and credibility of the organization and its officers. It is the factor that gives it its ‘oomph’ and saleability, and without the power of the Brand, an IPA becomes an also-ran.

Thus, the valuation of an IPA cannot be done solely on a fiscal basis. All the perspectives mentioned above must be calculated and counted. While the financials remain an important aspect of any valuation, they certainly are not the most important, or even, the largest component of a BSC for an IPA. At best, the fiscal status of an IPA can be used only if the organization scores a 100 on all other measures on its scorecard. At worst, the financials have to be completely discarded if the basics of business are not in place. We have seen that recently when a Fortune 500 corporation refused to take ownership or invest in an IPA solely because there were lawsuits against it for reasons of compliance.

The fundamentals of an IPA still remain the state of its compliance, the strength of its relationships and services, its feedback systems, employees, data and processes. Without these in place and sealed protectively, all one shall find is a house of cards. And the big problem with a house of cards is that the bigger it gets, the more vulnerable it becomes to sudden collapse. An IPA has to be based on an extremely strong foundation even though it needs to be nimble and flexible as regulations change and payment methodologies vary as we have seen with CMS in recent years.

When we measure the Business Process Perspective, we should measure the MRA, HEDIS, HOS, CAHPS and care management analyses, along with length of stays, continuity of care, ER visits, close follow-ups on nursing homes and hospitals, and post-acute care and post discharge care. The Operational metrics would also study the infra-structure, the state of IT, web services, reporting and sharing of information among the executives and owners.

The Customer Perspective should pay close attention to physician and employee satisfaction and retention, response rates and reputation. When practices are not wholly owned, this becomes an even more serious concern for any IPA. Also, the strength and managed care savvy of affiliates and risk of losses due to poor utilization by them cannot be ignored. If the IPA does not see itself as a fiscal intermediary and does not have adequate protections against a downturn and that it is in a risk business where the Pareto rule can get easily skewed from 20-80 to 1-99 and if the reserves are not strong or re-insurance is weak, all the juggling of numbers is of scarce significance.

An IPA is not any stronger by randomly signing up affiliates without interest, aptitude or drive to master managed care; in fact, the very opposite is true. Without proper infra-structure in place, an IPA should not attempt to grow. The continuous education and training of its employees is a sine qua non with any growth and a culture of compliance, quality and excellence should be a part of its DNA. The best IPA is a Learning Organization and a Knowledge-Creating Organization.

The concept of a Poison Pill in the valuation of any IPA is of much use. If the risk to the IPA due to significant legal or regulatory liability is high, it completely negates any financial valuation of the IPA almost like a junk bond and, in fact, may give it a negative status. We see this frequently in the market place when we see how the credit agencies appraise a company or a nation. Recently, we have seen how Universal Health Care, Inc, a Medicare Advantage plan, was taken over by a receiver thereby reducing its value to zero and with significant legal and financial liability to its executives and owners, when the Office of Insurance Regulations (OIR) decided that the plan was out of compliance. An IPA may come under the purview of the OIR too in a similar fashion.

Eventually, one must remember that any metric is only a reflection of an overall strategy, vision and mission, and the core competence of an IPA. If the IPA loses sight of these, no amount of tactical quantification would suffice in making it healthy and sustainable. Strategy must be integrated completely with the processes and the core strength of the entity should never be compromised. For if the core is forsaken, all is forsaken and the vitality of the organization may be irretrievably lost.

A poem by Dr. Singh:

The Sky

The sky covers my eyes

With white flares of zinc.

All desires are dissolved

In its trackless mind.

The sky fills my brain

With vast stretches

Of sun-lit spaces,

Clouds that float in silence

With wistful thoughts,

And stars that intuit

In brilliant scintillations

Of insight and wit,

Spread out in shapes

As varied as constellations,

Filled with the inner glow

Of presence as an amethyst

That fills within

With waves of trapped light.

The sky is a brain

That replaces my own.

DO NOT MISS OUR MARCH 19, 12:30 pm or APRIL 1, 5pm FREE 30 MINUTE WEBINAR ON Compounding Pharmacy Law.

For many medical practices this will be the best thing that has happened for them in years. Find out why and how during this informative webinar. Click here to register for the March 19 webinar. Click here to register for the April 1 webinar.

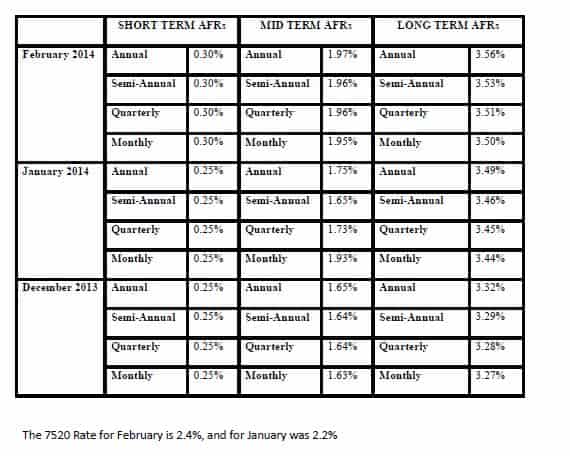

Applicable Federal Rates

Below we have this month, last month’s, and the preceding month’s Applicable Federal Rates, because for a sale you can use the lowest of the 3.

Seminars and Webinars

THE CLEARWATER BAR ASSOCIATION 444 SHOW – ASSET PROTECTION, ESTATE PLANNING AND LLC LAW UPDATE

Date: Thursday, February 27, 2014 | 4:00 p.m.

Location: Online webinar.

Speaker: Alan Gassman, Christopher Denicolo and Kenneth Crotty

Additional Information: To register for the webinar please visit www.clearwaterbar.org

******************************************************

THE JEST, THE SCGRAT AND THE E STREET SOFTWARE

Please join Alan Gassman, Ken Crotty and Chris Denicolo for a 30 minute webinar describing 2 new planning techniques and also free beta testing of the EstateView software that was developed by Gassman, Crotty & Denicolo, P.A.

Date: Tuesday, March 4, 2014 | 5:00 p.m.

Location: Online webinar

Additional Information: To register for the webinar please visit https://www2.gotomeeting.com/register/625212018.

******************************************************

FLORIDA BAR HEALTH LAW REVIEW 2014

Alan Gassman will be speaking on What Healthcare Lawyers Need to Know About Tax Law and Business Entities at this excellent annual Florida Bar conference that is attended not only by those who are taking the Board Certification exam but also healthcare lawyers and other advisors.

Other speakers will include Lester Perling who is the co-author of A Practical Guide to Kickback and Self-Referral Laws for Florida Physicians and a number of other books and publications, and Mickey Mouse, Donald Duck and the “dwarf planet” formerly known as Pluto!

Date: March 7 – 8, 2014

Location: Hyatt, Orlando, Florida

Additional Information: We thank Jodi Laurence and Sandra Greenblatt for all of their hard work in making this conference as successful as it is. For more information please contact Jodi at jl@flhealthlaw.com or Sandra at sg@flhealthlawyer.com.

******************************************************

TAX AND ASSET PROTECTION BASICS FOR THOSE WHO REPRESENT PHYSICIANS AND MEDICAL PRACTICES

Alan Gassman and Christopher Denicolo will be speaking at the Hillsborough County Bar Association’s Health Law Section Luncheon on the topic of Tax and Asset Protection Basics for Those Who Represent Physicians and Medical Practices.

Date: March 12, 2014

Location: Chester H. Ferguson Law Center in Tampa, FL

Additional Information: For additional information please contact Co-Chairs Sara Younger (sara.younger@baycare.org) or Thomas Ferrante (tferrante@carltonfields.com).

******************************************************

THE FLORIDA BAR LEADERSHIP ACADEMY: MARCH 2014 REGIONAL MEETING

On Saturday, March 15, 2014, Alan Gassman will join Judge Claudia Rickert Isom and Hillsborough County Bar Association President Susan E. Johnson-Valez for a panel discussion on the Benefits of Serving as a Community Leader. We welcome any and all questions, comments and suggestions for this presentation. We are developing a criteria worksheet that professionals can use to decide what the costs and benefits are of the many different non-billable activities and causes that we all have the opportunity to support.

Date: Saturday, March 15, 2014

Location: Marriott Tampa Airport

Additional Information: To register for the program please email agassman@gassmanpa.com

******************************************************

STRUCTURING JOINT EXEMPT STEP-UP TRUSTS: EMERGING TOOL TO MAXIMIZE STEP-UP IN BASIS

Date: Tuesday, March 18, 2014 | 1:00 – 2:30 p.m.

Location: Online webinar sponsored by Stafford Publications, Inc.

Speakers: Alan S. Gassman, Christopher Denicolo and Edwin P. Morrow, III, Esq.

Additional Information: To register for the webinar please visit https://www.straffordpub.com/products/structuring-joint-exempt-step-up-trusts-emerging-tool-to-maximize-step-up-in-basis-2014-03-18 or email agassman@gassmanpa.com

******************************************************

COMPOUNDING THE PROBLEMS AND OPPORTUNITIES FOR COMPOUNDING PHARMACIES

Date: Wednesday, March 19, 2014 at 12:30 p.m. or Tuesday, April 1, 2014 at 5:00 p.m.

Location: Online webinar

Speakers: Lester Perling and Alan Gassman

Additional Information: To register for the March 19, 2014 webinar please click here. To register for the April 1, 2014 webinar please click here.

******************************************************

COUNSELING SAME S*X COUPLES IN 2014

Alan Gassman will be speaking at the Wealth Council Florida Forum on Counseling Same S*x Couples in 2014

Date: Friday, March 21, 2014 | 10:30 – 12:00 p.m.

Location: Holiday Inn at the Orlando Airport

Additional Information: For more information and to register for the program please email agassman@gassmanpa.com

******************************************************

LUNCH TALK – LAW PRACTICE EFFICIENCY TIPS

Date: Monday, April 7, 2014 | 12:30 p.m.

Location: Online webinar

Speaker: Alan S. Gassman

Additional Information: To register for this webinar please visit www.clearwaterbar.org

******************************************************

FICPA SUNCOAST CHAPTER MONTHLY MEETING

Alan S. Gassman will be speaking at the FICPA Suncoast Chapter’s monthly meeting on the topic of THE FLORIDA CPA’S GUIDE TO PLANNING WITH PHYSICIANS AND MEDICAL PRACTICES

Date: Thursday, April 17, 2014 | 4:00 p.m.

Location: Tampa, Florida

Additional Information: For more information on this event please email agassman@gassmanpa.com or mary@clawsonasplus.com

******************************************************

DONOR LUNCHEON AT RUTH ECKERD HALL WITH PROFESSOR JERRY HESCH IN CLEARWATER, FLORIDA

Sponsored by Gassman, Crotty & Denicolo, P.A. Co-sponsors invited.

Professor Jerry Hesch will be speaking at a Donor Luncheon on the topic of CHARITABLE TAX SAVINGS: HOW TO MAKE SURE THAT UNCLE SAM CONTRIBUTES HIS SHARE TO MAXIMIZE RESULTS

Date: Tuesday, April 22, 2014 | TIME TO BE DETERMINED

Location: Ruth Eckerd Hall, Clearwater, Florida

Additional Information: For additional information please contact Suzanne Ruley at sruley@rutheckerd.net or Alan Gassman at agassman@gassmanpa.com

******************************************************

RUTH ECKERD HALL PLANNED GIVING MEETING

Professor Jerry Hesch will be speaking at the Ruth Eckerd Hall Planned Giving Meeting in Clearwater, Florida on the topic of INNOVATIVE CHARITABLE GIVING TECHNIQUES FOR THE WELL TUNED ESTATE PLANNER

Sponsored by Gassman, Crotty & Denicolo, P.A. Co-sponsors invited.

Date: Tuesday, April 22, 2014 | 4:00 p.m.

Location: Ruth Eckerd Hall, Clearwater, Florida

Additional Information: This session qualifies for 1 hour of continuing education credit for lawyers and CPA’s. To attend please email Suzanne Ruley at sruley@rutheckerd.net or Alan Gassman at agassman@gassmanpa.com

******************************************************

1st ANNUAL ESTATE PLANNER’S DAY AT AVE MARIA SCHOOL OF LAW

Speakers: Speakers will include Professor Jerry Hesch, Jonathan Gopman, Alan Gassman and others.

Alan Gassman will cover speak on Using Estate Planning Techniques to Optimize Family Wealth Preservation.

Date: April 25, 2014

Location: Ave Maria School of Law, Naples, Florida

Sponsors: Ave Maria School of Law, Collier County Estate Planning Council and more to be announced.

Additional Information: For more information on this event please contact agassman@gassmanpa.com.

******************************************************

THE FLORIDA BAR ANNUAL WEALTH PROTECTION SEMINAR

Date: Thursday, May 8, 2014

Speakers: Speakers will include Barry Engel on Offshore Trust Planning and Developments Over the Past 2 Years in Asset Protection, Howard Fisher and Alex Fisher on “Designer Entities – The Cutting Edge in Asset Protection”, Denis Kleinfeld on The Roadmap to Wealth Protection Planning and Alan Gassman on Structuring Business and Investment Assets and Entities – Wealth Protection 401 for the Dedicated Planner.

Location: Hyatt Regency Downtown, Miami, Florida

Additional Information: For more information please contact agassman@gassmanpa.com

******************************************************

40th ANNUAL NOTRE DAME TAX & ESTATE PLANNING INSTITUTE

Date: November 13 and 14, 2014

Location: Century Center, South Bend, Indiana

We welcome questions, comments and suggestions on variable annuities, which will be Alan Gassman’s topic for this conference.

Additional Information: The focus of this year’s institute will be on “Business Succession Planning: An Income Tax, Estate Tax and Financial Analysis.” As in past years, several sessions are designed to evaluate certain financial products and tax planning techniques so that the audience can better understand and evaluate these proposals in determining not only the tax and financial advantages they offer, but also evaluate limitations and problems they may cause in the future. Given that fewer clients will need high-end estate tax planning with the $5 million exemptions, other sessions will address concerns that all clients have. For example, a session will describe scams that target elderly individuals and how to protect the elderly from these scams. As part of the objective on refreshing or introducing the audience to areas that can expand their practice, other sessions will review the income tax consequences of debt cancellation, foreclosures, short sales, the special concerns that arise in bankruptcy and various planning available to eliminate the cancellation of debt income or at least defer it with a possible step-up basis at death. The Institute will also continue to have sessions devoted to income tax planning techniques that clients can use immediately instead of waiting to save estate taxes far in the future.