The Thursday Report – 1.2.2014 – New Year 2014 Edition

Everything You Always Wanted to Know About Motor Vehicle Ownership Planning* and Did Not Think To Ask – Part 1

Medical Practice Wisdom by Dr. Pariksith Singh – Part 3 – Medicare Risk Adjustment: Coding and Concepts

Basic Asset Protection for Doctors: Creditor Exempt Assets and Fraudulent Transfer Rules – Part 3 of a 3 Part Series by Alan S. Gassman

What is an ISC? Federal Deposit Insurance Options for Accounts Over FDIC’s $250,000 Guarantee Limits

Not Again, Colonel – AGAIN! – An Update on How to Remove a Mug Shot From Google in 48 Hours for as Little as $99

Ode to the Largo Commissioners

We welcome contributions for future Thursday Report topics. If you are interested in making a contribution as a guest writer, please email Janine Gunyan at Janine@gassmanpa.com.

This report and other Thursday Reports can be found on our website at www.gassmanlaw.com.

Everything You Always Wanted to Know About Motor Vehicle Ownership Planning* and Did Not Think To Ask, Part 1 of a 4 Part Series

Part 2 on 1.9.2014 will discuss auto insurance issues and using subsidiary entities to own and operate vehicles to limit liability.

Part 3 on 1.16.2014 will discuss special planning for children and ownership issues.

Part 4 on 1.23.2014 will discuss survivorship planning and why boats and airplanes are different.

INTRODUCTION

Virtually all clients own and operate motor vehicles, which are by far the greatest liability generators in Florida. Multi-million dollar jury verdicts coupled with owner liability and parent-child liability concepts make motor vehicle liability prevention planning an essential part of any individual or corporate representation. This article provides a basic framework for lawyers representing individuals and businesses who own and/or operate motor vehicles.

Basic considerations which must be evaluated with respect to motor vehicle planning include the following:

a. The owner of an automobile is responsible for a permissive driver’s negligence, subject to certain limitations described below.

b. An individual who signs a contract with the state to permit a minor to receive a driver’s license is absolutely responsible for the minor’s negligence.

c. Through proper planning a motor vehicle may be owned by a corporation and driven for business purposes, thus permitting tax deductibility thereof.

d. Upon purchasing a motor vehicle, Florida state sales tax will be incurred, except to the extent of consideration attributable to trade-in allowances where the trade-in has come from the same person or entity who takes title to the newly purchased vehicle.

e. A motor vehicle can be a valuable asset and thus subject to creditor claims, probate proceedings, and other property rights considerations.

f. Liability insurance and costs of coverage for different ownership arrangements are often the “tail that wags the dog” in vehicle planning.

The most important planning consideration for a majority of clients revolves around limiting liability for driver negligence.

STRICT LIABILITY FOR OWNERS UNDER THE DANGEROUS INSTRUMENTALITY RULE

In Florida, individuals who own automobiles may be shielded from strict liability by statute if the owner allows another (a permissive user) to drive the vehicle. If a driver has at least $500,000 of liability insurance coverage, an individual automobile owner is only liable for up to $100,000 per person, up to $300,000 per incident for bodily injury, and up to $50,000 per incident for property damage. However, if the permissive user does not have liability insurance coverage, then the individual owner may be liable for an additional $500,000 in economic damages, but the economic damages responsibility is reduced by amounts actually recovered from the driver and from any insurance or self-insurance covering the driver. For the complete text of Florida Statute Section 324.021(9)(b)(3).

Owner liability emanates from the “Dangerous Instrumentality Doctrine,” which provides that the owner of a dangerous instrumentality is liable for the negligent acts of a person who uses it with the owner’s actual or implied consent. In Florida, the doctrine extends to negligence of someone who borrows the vehicle from someone else who had permission to borrow the vehicle from the owner. For instance, in Fischer v. Alessandrini, a father lent his truck to his son, who then lent the truck to another party, who collided with Alessandrini. There, the father was allowed to limit his liability under Florida Statute Section 324.021(9)(b)(3).3 Further, a vehicle owner’s auto insurer is primarily liable to persons injured as a result of the negligence of a person operating the owner’s vehicle with the owner’s permission. Even in situations like Fischer, where a second permissive user is involved, the owner’s carrier will be primarily liable to the injured parties.

A possible issue is that the statute only covers individual owners. It may not explicitly cover joint owners. If it does cover joint owners, then it is unclear whether the $800,000 limit on liability will apply to both owners to create a joint liability of $1,600,000. This question will be discussed in more detail below. This is why it is often recommended that when spouses purchase a vehicle, the spouse least exposed to liability should take title to the vehicle and the more “at risk” spouse should drive it. In Florida, motor vehicle liability insurance policies cover the owner of the vehicle and any other driver whom the owner gives actual or implied consent, thus protecting a spouse not named on the title.

Further, there are no assurances that this statute would have any affect whatsoever if the negligent operation of the vehicle occurs outside of Florida.

Finally, the statute only applies to an owner who is a “natural person,” thus rendering the provision inapplicable where the vehicle is owned by a business entity. Also the statute does not shield an owner from liability for NEGLIGENT ENTRUSTMENT or for having “signed” with the State of Florida to be responsible for a minor driver.

NEGLIGENT ENTRUSTMENT

In Florida, the doctrine of negligent entrustment of a dangerous instrumentality applies to motor vehicles. The owner of a motor vehicle has a nondelegable duty to ensure that the vehicle is operated safely. Florida Statute Section 324.021(9)(b)(3) does not limit liability for negligent entrustment or negligent maintenance. The cause of action for negligent entrustment exists where the car owner knew, should have known, or had reason to know that the person borrowing the car was incompetent, unfit, inexperienced, or reckless; that the entrustment created an appreciable risk of harm to others; and that the harm to the injured victim was proximately caused by the negligence of the entrustor.

LIABILITY OF TWO PEOPLE WHO JOINTLY OWN A CAR

Although Florida Statute Section 324.021(9)(b)(3) limits a car owner’s liability if a permissive user is involved in an accident, as mentioned above, what happens when two people own the car? Is the limited liability a higher amount? Are they liable for twice as much? Does the victim of the accident benefit because there are two owners?

These particular questions have not yet been addressed by Florida courts. However, in Rouse v. Greyhound Rent-A-Car, the Fifth Circuit decided a case on appeal from the Middle District of Florida, which held that where there were two owners of a vehicle, the owners were jointly liable for the payment of damages to the injured party. The Fifth Circuit reversed the district court because it found that one of the “owners” was not in fact an owner, and thus he was not subject to joint liability. But the court did not address the reasoning of the district court concerning joint liability by two owners. Therefore, since it appears that all the owners would be jointly liable for the amount for which only one owner would be liable, it seems plausible that their liability would also be limited to the amount proscribed by the limiting-liability statute.

Public policy would dictate the same result. Just because a car driven by a permissive user is owned by two people does not mean that the injured victim of a car accident by that jointly owned car driven by the permissive user should benefit and be entitled to a higher amount of damages. This would deter individuals from putting more than one name on the title of a car and indicating joint ownership.

Medical Practice Wisdom by Dr. Pariksith Singh – Part 3

Medicare Risk Adjustment: Coding and Concepts

Most advisors and almost all physicians are well aware of traditional Medicare and health plan coding, whereby Medicare and the health plans pay doctors based upon numeric codes that indicate services rendered.

Far fewer physicians and advisors understand the MRA score system which stands for Medicare Risk Adjustment. Medicare gives monies to HMO’s to provide turn-key care for Medicare patients to sign up for the HMO system, which is known as Medicare Advantage Plan. The sicker the patient is, the more money that gets paid for this turn-key care. It therefore behooves physicians who are paid based upon the amount the government puts up and the health plans to use the highest MRA code possible, but to not use inappropriate MRA codes.

Dr. Singh does a great job this week in discussion of MRA codes and matters associated therewith.

To understand Medicare Risk Adjustments (“MRA”), one may wish to understand where health care is moving. In my mind, MRA as part of coding is as integral to standardizing health care, auditing, billing and collections, such as Current Procedural Teminology or International Classifications of Diseases, Star rating, Physician Qualify Reporting System, HEDIS criteria, and etc. We are seeing greater objectivization and benchmarking in services that had until now been subjectively evaluated for efficiency and results.

What does this do to the normal practice? It gives, at first glance, the opportunity to compare apples to apples. Thus, if each health care service can be measured on the same terms, such as severity of illness, intensity of intervention, goals achieved, customer service, compliance, and utilization management, there is an even playing field where everyone becomes equal. However, it appears that this now counter-intuitively pits apples against lemons. The “lemons” are those practices who refuse to play catch up, refuse to learn documentation and coding, and insist on staying with old-fashioned beat-up path of health care that has failed miserably in the past.

However, for those who are willing to stay ahead of the curve, this is a chance to shine not only as apples but as the finest and select pièce de résistance fruit on the table. Simply put, it is the chance for those who are nimble, eager to learn, and willing to put processes in place that improve and measure health services to blaze the trail and take the lead in the health care industry. Those who stay behind will be road-kill. This may be shocking and sound stark, but the market can be unforgiving, and the business model of the new health care is ruthless.

No longer will the provider be given unlimited powers and complete freedom to code and bill as they deem fit. If services for home health care, Skilled Nursing Facilities, and hospital care are to measure up to this strict criterion, the provider will be put to test. And if they are not prepared for the new demands of the system, there might be significant penalties or losses from recoveries by the government.

The old managed care had essentially fixed premiums, no matter how sick the patient was, and the only way to increase profits was to pay less to providers, improve contracts and utilization, or deny care by refusing to treat illnesses or dumping sicker patients (which used to be called cherry-picking the healthier population).

The newer managed care system paid more for sicker patients, for improved documentation, coding and billing, and ensuring that claims reached CMS via the HMO. The way to increase profits was not only to reduce expenses but also by increasing premiums (what might be called cherry-picking the sicker population).

The third wave in managed care introduces some more changes where Star Ratings, Customer Satisfaction, and HEDIS criteria become more and more important. The Star Rating system was developed by CMS to help consumers compare nursing homes more easily and held identify areas which a patient or their family would want to ask questions about. This third wave ties MRA to utilization for proper data reporting, review, and analysis. This, in turn, ties all of these requirements into a strong compliance system, care management, customer service, ACOs, and Medical Homes. This field is evolving rapidly, but providers can significantly overlap these several new initiatives which are overseen by the same agencies. It is no wonder why Florida Medical Quality Assurance is certifying Medical Homes, ACOs, the indicators for meaningful use, for the reporting criteria for Medical Homes and ACOs have significant similarities.

You cannot manage what you cannot measure. This is an old axiom, but this was the case under the older systems. However, now the government insists that it has created the tools to measure the efficacy of managed care and allow the more efficient practices to be more profitable and creates opportunities to save on wasted resources. So, the theory seems to be; however, in practice, what will separate the men from the boys (or women from the girls) will be a successful implementation of strong systems which will capture the MRA diagnoses correctly.

As we see the increasing standardization and objectivization of medical care, we will also see another phenomenon, which I call the “subjectivization of health care.” By this I mean, when parameters are created by which, in theory, one practice can be gauged against the next and these findings can be easily posted and shared on the internet and other media, customers will clamor for those practices which can be distinguished for going that extra yard by providing that additional touch of customer service or providing the “health care experience”, akin to the Disney experience or the Apple gestalt.

How to succeed with MRA? These are some of the basics that will need to be implemented in any practice that intends to “hang ten” on this third wave:

1) Constant education and training of the providers (including specialists), staff, auditors, and billers. Last but not least, the plan.

2) Creating a partnership with specialists, vendors, IT systems, and, again, the plan.

3) Implementing a system to retrospectively check the chart on a constant basis and bring codes forth.

4) Mandatory compliance training and certification of every employee at least annually.

5) Use a Utilization Management software and system that ties all the data together making it actionable and becomes the pivot for all the services provided to the patient whether it is inside or outside the practice.

6) A data collection system, including getting all the hospital records, discharge summaries, consults, labs, radiology reports, and other information into your client’s record.

7) Incentivizing physicians to improve the overall quality of care and compliance testing.

8) Focusing intensely on customer service and experience and educating the patients about their conditions and health care status.

9) Developing special needs plans and specialty clinics.

10) Getting a constant feedback from the plan about the MRA scores of the practice, patient by patient, and constant updating of one’s data portals.

A strong MRA push is part of the overall compliance program and cannot be ignored in this era of rising health care costs and decreasing revenues.

A Poem by Dr. Singh:

Experience without words

Is the door without walls

That opens you to worlds

You inhabit within

Thus thoughts lose relevance

And feelings their anchor

Choiceless one encounters

The world without distinction

Basic Asset Protection for Doctors: Creditor Exempt Assets and Fraudulent Transfer Rules – Part 3 of a 3 Part Series by Alan S. Gassman

Most physicians are aware that certain types of assets cannot be reached by creditors.

Most physicians are also aware that under the Federal Bankruptcy Rules an individual can file a Chapter 7 Bankruptcy, which can discharge the debt otherwise owed to a malpractice creditor, notwithstanding that the physician may be allowed to keep all of his or her creditor exempt assets.

Most physicians are also aware of the “Fraudulent Transfer Rules”, which can provide creditors with the ability to obtain otherwise exempt assets if these assets were purchased with non-exempt monies or other assets that were “converted” for the purpose of avoiding creditors.

Many clients are also aware that a bankruptcy discharge may not be received if a “fraudulent transfer” has occurred.

Many clients are also aware that a bankruptcy discharge may not be received if a “fraudulent transfer” has occurred within two years of the bankruptcy being filed.

The interaction of the above rules has important implications for the individual planning strategies employed by physicians under varying circumstances. To make this more complicated, the laws and interaction of State Law and Federal Bankruptcy Law are often uncertain, and subject to change. Further, bankruptcy judges will often “bend the rules” to arrive at results that they believe to be just.

The various “exempt assets” and some unique rules that apply to each of them are as follows:

1. The Homestead. The Florida Constitution strictly protects homestead property, being up to one half acre within city limits or up to one hundred and sixty acres if outside of the city limits. Properties that have a home plus other buildings or real estate not associated with the home may or may not be protected depending upon the circumstances.

The Constitutional protection of the homestead is so strong that under Florida Law a “fraudulent transfer” of monies into a homestead by purchase, mortgage paydown, or for improvements cannot be set aside in the Florida courts as a fraudulent transfer unless the monies transferred constitute stolen funds or are otherwise considered to be “contraband.”

Nevertheless, the Federal Bankruptcy Law was amended in 2005 to deny even Floridians the right to retain their homestead in a bankruptcy under certain circumstances:

a) If the homestead was acquired within three years and four months of the filing of the bankruptcy, except to the extent acquired from the proceeds of the sale of a prior homestead that was owned within such time parameters.

b) To the extent that funds put into the homestead as a “fraudulent transfer” within ten years of filing of the bankruptcy.

c) Where the bankrupt individual has a judgment against him or her based upon gross negligence, willful misconduct, or corporate fraud or certain white collar crime related matters.

As a consequence of the new Federal Bankruptcy Law, many physicians are well advised to pay their home mortgages down earlier rather than later, contrary to prior advice that was given before the bankruptcy law was passed.

What is an ISC? Federal Deposit Insurance Options for Accounts Over FDIC’s $250,000 Guarantee Limits

In the US, bank depositors are protected by the FDIC, or Federal Deposit Insurance Corporation. This independent US agency protects up to $250,000 per a depositor. But what if your account is over $250,000? What if it is in the millions?

Promontory Interfinancial Network, LLC has developed several services for those individuals with cash assets of over $250,000: CDARS and ICS. These services utilize the FDIC protections by separating funds into several different accounts at other banks. However, while the funds may be in several banking institutions, the account owner is kept completely confidential with the original bank. The service also provides the ease of one statement for the account owner.

Previously, we reported on CDARS, the Certificate of Deposit Account Registry Service, which protects multi-million-dollar CD deposits, while allowing the deposits to earn an often favorable interest rate. Click here to view that Thursday Report.

With an ICS, or Insured Cash Sweep, money is placed into an ICS Account. The account owner has two options: a Savings or a Demand Account. Demand deposit accounts have a deposit interest rate, and the Money Market Deposit Account Interest is available with the savings option.

Once one or both account options are selected, the money is then separated into bundles of less than $250,000, and placed at separate ICS banking institutions. This way the bundles can earn interest, and still be covered by the FDIC limit of $250,000.

Although separated, the accounts are on one monthly banking statement, and the client is able to treat it as one account. The money can be withdrawn within 24 hours, and for the ICS Savings Account, you can only withdraw six times a month.

With ICS, the bank is the custodian for the funds, but the funds also have a sub-custodian: The Bank of New York Mellon.” The disadvantage is that right now ICS has very little return.

Some individual banks also have their own insured bank deposits. For instance, BB&T has IDP, an Insured Deposit Program that is limited to $1,750,000. Edward Jones has an Insured Bank Deposit that provides coverage for savings accounts up to $1.5 million depositor.

Not Again, Colonel – AGAIN! – An Update on How to Remove a Mug Shot From Google in 48 Hours for as Little as $99

In May we ran an article called “Not Again, Colonel! – How To Remove A Mug Shot From Google In 48 Hours For As Little As $99.” (Click here to view the article.) This month we are re-running the article with an addition for removing your client from other public search engine services.

—

Sometimes bad things happen to good colonels. And sometimes good colonels make mistakes. Unfortunately these types of situations can result in an arrest and mug shot, like the Colonel’s above. Regardless of innocence or guilt, mug shots often end up online and can appear when someone searches an arrested person’s name. This can be very harmful in many situations, such as when someone is searching for a new job or deciding which fried chicken proprietor to visit. Well do not fear. The Thursday Report has found a cheap and quick way to stop mug shots from appearing in Google searches. Read on for details.

In most counties in Florida, the county sheriff’s office will make mug shots available online. Most county sheriff’s websites have a feature where you can search to see if a person has ever been arrested. If the person has been arrested, then the county sheriff’s website will usually display details of the arrest and a mug shot. But the good thing about most county sheriff’s office websites is that the arrest information and mug shots normally do not show up in a regular Google search for a person’s name.

The real problem is third party websites like www.mugshots.com and www.florida.arrests.org. These types of websites take the mug shots from county sheriff’s office websites and then publish the mug shots on their own website. Mug shots on these third party websites will then show up in regular Google searches and Google image searches.

Fortunately, there are services that can stop a mug shot from showing up in a Google search. We do not know how they do it, but they work. We also do not know if the mug shot websites and the removal services are in cahoots, but we would be very interested if someone looked into this.

An online search for “mug shot removal service” will yield a number of different companies offering the service. We have found one website that works well and is very inexpensive: RemoveMyMug.com. We do not endorse this website or have any affiliation with RemoveMyMug.com; we can only say that it has worked in the past for us. We cannot get into details, but the Thursday Report has a “checkered” past.

RemoveMyMug.com costs $99 per mug shot removal. This means that you will have to pay $99 for each website that displays a mug shot. RemoveMyMug.com claims they typically take 24 hours or less for a removal, with some taking only minutes. They also offer a money back guarantee if they are unsuccessful.

Once the mug shot removal service removes the mug shot, the Google search result will not disappear automatically. Eventually Google will see that the link to the mug shot website no longer works and eliminate all search results. Until then, the mug shot listing will appear in Google’s search results, but if someone clicks on the search result they will receive a message that the page is no longer available. This is called a dead link. Google’s removal process can take anywhere from one to thirty days. But it is possible to make the dead link disappear in a few hours.

Google allows people to report dead links, like a removed mug shot. To do this, first you go to the Google content removal page. Click here for the page. Click on the option that says “Remove content that’s not live.” Then log in using a Google account. You can make one up if you do not already have one. After that you will see a button in the middle of the Google webpage that says “Create a new removal request.” Click on this button and paste the URL for any mug shot webpage that was deleted. The easiest way to do this is to open a second webpage or browser, perform a Google search for the person’s name, and then copy and paste any search results that are showing. We have found that Google will often remove a dead link in just a few hours.

That should take care of any Google search results. If you or your client are interested in expunging an arrest record, then you should check individual county websites to learn how to do so.

ADDITION:

InstantCheckMate.com is a paid service that searches and compiles public records on an individual. This includes current and former addresses, criminal records, and sex offender databases. Service charges range from $29.95 for a single report, to monthly memberships. We were able to get a 5 day unlimited trial for $1.00 by exiting out of the payment options page (you can also google “instantcheckmate.com trial membership” to get a trial rate). The catch is to cancel the membership, you must call customer service. Otherwise you will be billed the full membership amount that automatically renews.

It is free to enter a name and a listing of the search results for the name, which includes any cities the person has lived in and will sometimes display an exclamation point next to the name. We ended up having to call InstantCheckMate.com to find out what this exclamation meant, since the website does not tell you. It simply means the information is being updated, and the county clerk is doing something with the individual’s name; however, our first instinct was it involved criminal actions, since the website advertises “Police Records, Mugshots, Contact Information and Much More!”

If you purchase the service to view the individual record, it will show any public information on an individual, including any arrests regardless of whether the charges were dropped. It will also include prior addresses (with aerial photographs of residences), an individual’s birth date, astrology sign, licenses, marriage/divorce records, related persons (including business associates and roommates), and sex offenders living near the individual’s address.

Fortunately, information can be removed from the website by going to http://www.instantcheckmate.com/optout. There are two ways to remove information. Option 1 is to mail a request to Instant Checkmate’s physical address in Las Vegas. The information will be removed within 3-7 days after Instant Checkmate receives your request. Option 2 is an expedited Opt Out, which includes a form which is submitted on the website. This option takes 48 hours to remove the information. The catch is that the information must be entered exactly as it appears on the website, and you are only allowed a limited number of submissions with a single e-mail address. If an individual has multiple listings, then each listing must be submitted.

After submitting an opt out request, InstantCheckMate.com will send a confirmation e-mail, with a link to finalize the request. After finalizing the request, it takes 48 hours for the entire listing to be removed.

InstantCheckMate.com is just one of many services available to the public to access information. We found the customer service to be pleasant, and did not have any problems cancelling a trial membership after submitting opt out requests. The entire listing was promptly removed after submitting an expedited opt out request.

It is important to actively review your search results, especially if you have any criminal records, even if the charges were dropped.

ODE TO THE LARGO SEPTIC COMMISSION

We have lots of neat things in Kent Place,

Including fresh poop that gets in your face,

When driving in from Belcher the smell is strong,

Much worse than the sulphur water that might help a lawn,

But it is fun to see and smell the pumping

Each Friday evening,

As Sabbath comes in,

Our rabbi is leaving

(he is moving to Flushing, NY).

There’s a problem with the pipes,

That we don’t understand,

And that can’t be fixed,

Despite the demand,

And the damages to the coyotes,

Is of concern,

They’ve asked us for incense,

That they can burn,

And barking “Arff please,

Spare us from disease.”

As values go down,

Our taxes will too,

So we can afford gas masks,

And have bought quite a few,

And we reached out to Fidel,

So he is sending a crew,

To save us from sewage,

And democracy too.

Yes the problem is big,

And our choices limited,

Are we confused,

Or are the systems demented?

So last Tuesday,

We went to see,

How the commissioners would handle

Our poop and our pee.

What we heard last Tuesday,

Was frustrating and tough,

Mostly they didn’t know,

And their engineer cannot do enough.

So to Mayor and commissioners,

Thank you for being good listeners,

We hope you will act anew,

So that the sewage doesn’t end up on you.

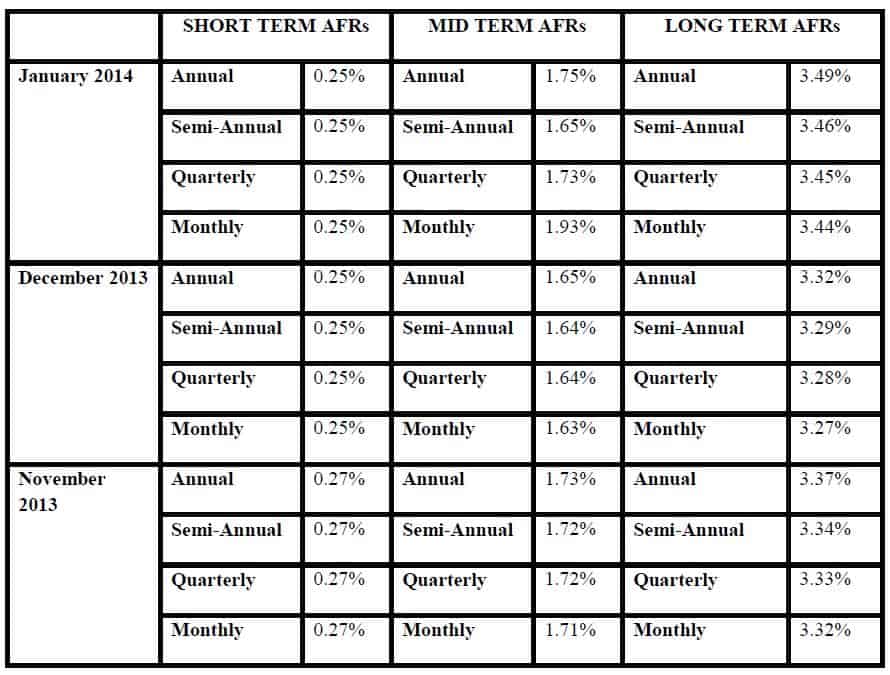

Applicable Federal Rates

Below we have this month, last month’s, and the preceding month’s Applicable Federal Rates, because for a sale you can use the lowest of the 3.

The 7520 Rate for January is 2.2% and for December was 2.00%.

Seminars and Webinars

THE FLORIDA BAR – REPRESENTING THE PHYSICIAN

Date: Friday, January 17, 2013

Location: The Hyatt Hotel, Orlando, Florida

Additional Information: The annual Florida Bar conference entitled Representing the Physician is designed especially for health care, tax, and business lawyers, CPAs and physician office managers and physicians to cover practical legal, medical law, and tax planning matters that affect physicians and physician practices.

This year our 1 day seminar will be held in the Hyatt Hotel near Walt Disney World.

A dinner for the Executive Committee of the Health Law Section of The Florida Bar and our speakers will be held on Thursday, January 16, 2013, whether formally or informally. Anyone who would like to attend (dutch treat or bring wooden shoes) will be welcomed. Your tax deductible hotel room to start a fantastic week near Disney, Universal, Sea World and most importantly Gatorland, can include a room at the fantastic Hyatt Hotel for a discounted rate per night, single occupancy.

PINELLAS COUNTY CHAPTER OF THE FLORIDA ASSOCIATION OF WOMEN LAWYERS SEMINAR

Alan Gassman will be speaking on Same Sex Marriage and Associated Laws We Should All Know About Anyway.

Date: January 30, 2014 | 5:30 p.m.

Location: Stetson Law School, Gulfport, Florida

Additional Information: For more information on this event please contact agassman@gassmanpa.com.

FLORIDA BAR HEALTH LAW REVIEW 2014

Alan Gassman will be speaking on What Healthcare Lawyers Need to Know About Tax Law and Business Entities at this excellent annual Florida Bar conference that is attended not only by those who are taking the Board Certification exam but also healthcare lawyers and other advisors.

Other speakers will include Lester Perling who is the co-author of A Practical Guide to Kickback and Self-Referral Laws for Florida Physicians and a number of other books and publications.

Date: March 7 – 8, 2014

Location: Hyatt, Orlando, Florida

Additional Information: We thank Jodi Laurence and Sandra Greenblatt for all of their hard work in making this conference as successful as it is. For more information please contact Jodi at jl@flhealthlaw.com or Sandra at sg@flhealthlawyer.com.

HILLSBOROUGH COUNTY BAR ASSOCIATION HEALTH LAW SECTION LUNCHEON

Alan Gassman and Christopher Denicolo will be speaking at the Hillsborough County Bar Association’s Health Law Section Luncheon on the topic of Tax and Asset Protection Basics for Those Who Represent Physicians and Medical Practices

Date: March 12, 2014

Location: Chester H. Ferguson Law Center in Tampa, FL

Additional Information: For additional information please contact Co-Chairs Sara Younger (sara.younger@baycare.org) or Thomas Ferrante (tferrante@carltonfields.com).

1st ANNUAL ESTATE PLANNER’S DAY AT AVE MARIA SCHOOL OF LAW

Speakers: Speakers will include Professor Jerry Hesch, Jonathan Gopman, Alan Gassman and others.

Date: April 25, 2014

Location: Ave Maria School of Law, Naples, Florida

Sponsors: Ave Maria School of Law, Collier County Estate Planning Council and more to be announced.

Additional Information: For more information on this event please contact agassman@gassmanpa.com.

THE FLORIDA BAR ANNUAL WEALTH PROTECTION SEMINAR

Date: Thursday, May 8, 2013

Speakers: Speakers will include Barry Engel on Offshore Trust Planning and Developments Over the Past 2 Years in Asset Protection, Howard Fisher and Alex Fisher on “Designer Entities – The Cutting Edge in Asset Protection”, Denis Kleinfeld on The Roadmap to Wealth Protection Planning and Alan Gassman on Structuring Business and Investment Assets and Entities – Wealth Protection 401 for the Dedicated Planner.

Location: Hyatt Regency Downtown, Miami, Florida

Additional Information: For more information please contact agassman@gassmanpa.com

NOTABLE SEMINARS PRESENTED BY OTHERS:

48th ANNUAL HECKERLING INSTITUTE ON ESTATE PLANNING SEMINAR

Date: January 13 – 17, 2014

Location: Orlando World Center Marriott, Orlando, Florida

Sponsor: University of Miami School of Law

Additional Information: For more information please visit: http://www.law.miami.edu/heckerling/

16th ANNUAL ALL CHILDREN’S HOSPITAL ESTATE, TAX, LEGAL & FINANCIAL PLANNING SEMINAR

Date: Wednesday, February 12, 2014

Location: All Children’s Hospital Education and Conference Center, St. Petersburg, Florida with remote location live interactive viewings in Tampa, Sarasota, New Port Richey, Lakeland, and Bangkok, Thailand

Sponsor: All Children’s Hospital

THE UNIVERSITY OF FLORIDA TAX INSTITUTE

Date: February 19 – 21, 2014

Location: Grand Hyatt, Tampa, Florida

Presenters: Martin McMahon, Jr., C. Wells Hall, III, Abraham N.M. Shashy, Karen L. Hawkins, Lawrence Lokken, Stephen F. Gertzman, James B. Sowell, John J. Rooney, Louis Weller, Ronald Aucutt, Karen Gilbreath Sowell, Herbert N. Beller, Peter J. Genz, Stephan R. Leimberg, John J. Scroggin, Lauren Y. Detzel, David Pratt and Samuel A. Donaldson

Sponsor: UF Law alumni and UF Graduate Tax Program

Additional Information: Here is what UF is saying about the program on its website: “The UF Tax Institute will provide tax practitioners and other leading tax, business and estate planning professionals with a program that covers the most current issues and planning ideas with a practical, informative, state-of-the-art approach. The Institute’s schedule will devote separate days or half days to individual income tax issues, entity tax issues and estate planning issues. Speakers and presentations will be announced as the program date nears to ensure coverage of the most timely and significant topics. UF Law alumni have formed the Florida Tax Education Foundation, Inc., a nonprofit corporation, to organize the conference.”